Retirement Plan for Faculty and Staff

Investment & Contribution Elections

-

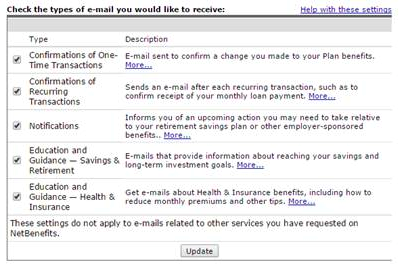

I made my investment selections in NetBenefits, but I did not receive a confirmation email. Why?

You may have turned off confirmation messages in your email setting preferences. To change your settings, log in to NetBenefits, click "Your Profile" at the top, and then select "E-Mail Settings" from the left preferences menu. Check the box next to the type of confirmations or emails you would like to receive, and then click the "Update" button at the bottom of the screen. You can also verify Fidelity has the correct email address on file at the top of the E-Mail Settings page.

Costs & Fees

-

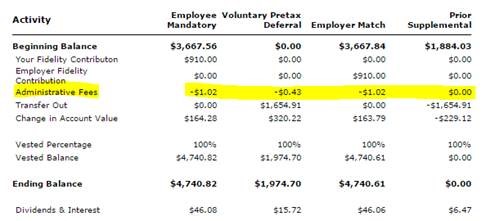

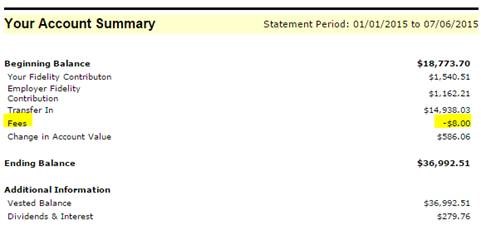

How will the recordkeeping fee be charged and appear on my statement?

The recordkeeping fee is charged quarterly and listed as Fees in your account summary:

You may also see it listed as Administrative Fees in the Account Activity section of your statement. The fee is proportionally divided among contribution types: